Executive Summary

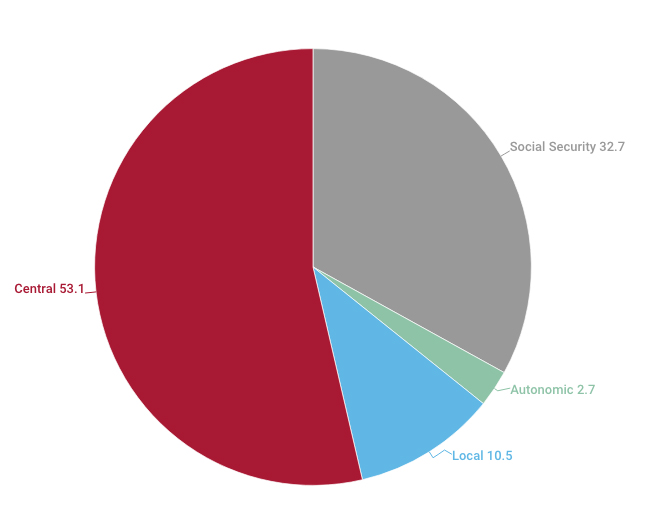

Fiscal Liberation Day, Tax-Free Day or Tax Freedom Day is the date on which a given society has generated enough income to cover all tax obligations. From then on it is when we no longer work for the State and start earning money for ourselves. This day translates the tax pressure into the number of days needed to pay direct and indirect taxes, as well as Social Security contributions. Of the 119 days worked in 2010 to deal with all taxes, 53.1 were dedicated to the Central Administration; 22.7 to the Autonomous; 10.5 to Local and 32.7 to Social Security.

Graph 1. Breakdown of the number of days spent to comply with the tax authorities

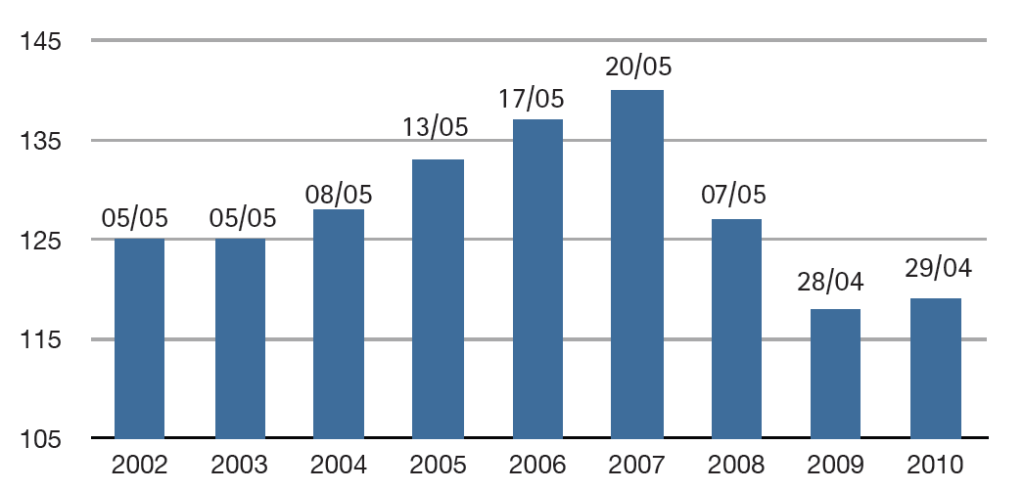

In the last nine years, tax pressure in Spain has been increasing. Whereas in 2002 the Tax Freedom Day arrived on May 5, in 2007 it was delayed until May 20. Despite this upward trend, in the last three years the tax freedom day changed course and retracted to April 28 in 2009 and April 29 in 2010; that is, 21 days earlier than in 2007, when we worked the most for the State and the least for ourselves and our families.

The reversal of this trend is not due to reductions in tax rates, but to the fall in economic activity. The 2008 crisis has substantially reduced the collection capacity of all tax authorities. Those taxes linked the most to economic activity, such as VAT and Corporate Tax, are the ones that have suffered most, followed by the Income Tax for Individuals (Spanish personal income tax). In 2010, the increase in the tax rates of VAT and Special Taxes has led to an increase in the collection of both taxes, but revenues are still far from those achieved in the 2007-2008 period. Meanwhile, the collection of the remaining taxes has further contracted. Therefore, the aforementioned increases in tax rates have only delayed Spain’s Tax Freedom Day 24 hours, while the contraction of economic activity between 2007 and 2009 advanced this date by 22 days without the rates being reduced.

Graph 2. Tax Freedom Day in the period 2002-2010

Graph 3. Tax Freedom Day 2011

Once again the effects of the treacherous Laffer Curve are tested: a rise in rates does not always translate into higher tax revenues or an increase in expected revenues.

Although tax rates are very similar from one autonomous community to another, the tax pressure and the tax freedom day greatly differ: from March 13 in the Canary Islands to July 23 in the Community of Madrid. These variations reflect the wide spectrum of factors that influence tax pressure, from the Gross Domestic Product (GDP) to the existing unemployment rate in each region, through the diversification and type of economic activity and even the headquarters of some multinationals. In 2010, the last Autonomous Communities to be freed from tax obligations were Madrid, Cantabria and Catalonia. Their tax freedom day came later than the national average, which was April 29.

However, we must carefully analyse the case of Madrid. Tax pressure has risen in the capital city because it is where large companies and multinationals have their headquarters, but it does not translate into higher levels of taxes on residents. In fact, the tax pressure exerted by the Autonomous Administration is in line with the average of the others, while the regional expenditure in relation to GDP is the smallest in Spain.

However, the Central Administration collects through the Madrid delegation of the Tax Agency many Special Taxes, VAT and, to a lesser extent, Corporate and Income Tax. The Autonomous Communities (CCAA in Spanish) with lower tax pressure and, therefore, the first which celebrated the tax freedom day in March were: Canary Islands, Castilla y León, Extremadura, La Rioja and Murcia. These are followed by those CCAA with moderate tax pressure. These had their tax freedom day in April, and were Andalusia, Galicia, Balearic Islands, Aragon, Castilla La Mancha, Valencia, Asturias, Navarra and the Basque Country. If we analyse the 2009-2010 period, out of the 17 CCAA, only seven increased the tax pressure with the increase in tax rates, while the others continued to reduce their tax collection against their GDP. This shows that increases in tax rates have adverse effects to those expected depending on the region.

Tax Freedom Day in Europe

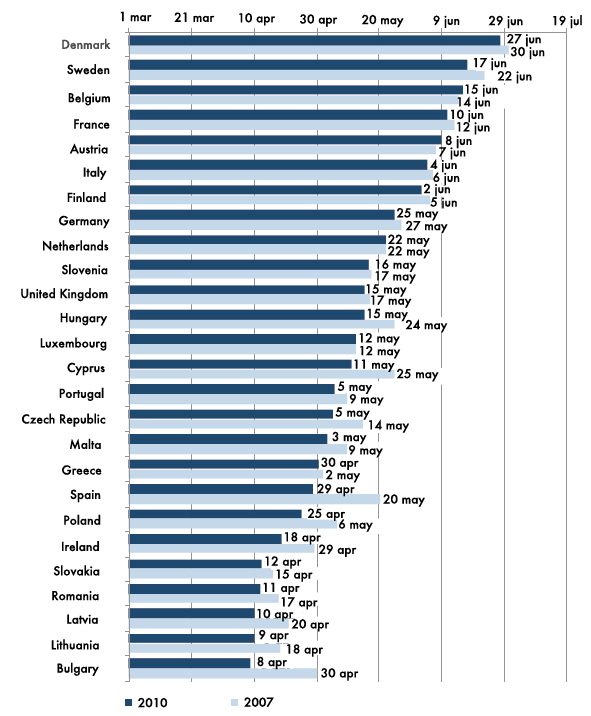

Whereas in 2010 the Tax Freedom Day arrived at the end of April, placing Spain relatively soon in the European context, the situation before the economic crisis was quite different. In 2007, Tax Freedom Day was celebrated in Spain 21 days later (May 20) than in 2010, with a medium-high tax pressure, placing it in the twelfth place of the 26 countries analysed.

Graph 4. Tax Freedom Day in Europe 2007-2010

Today, Finland, Italy, Austria, France, Belgium, Sweden and Denmark are countries where more days are worked for the State, so that the Tax Freedom Day arrives in the middle of the year, in the month of June. These are followed by Malta, the Czech Republic, Portugal, Cyprus, Luxembourg, Hungary, the United Kingdom, Slovenia, the Netherlands and Germany that celebrate their tax freedom day in May. Due to the crisis and the shadow economy, tax collection has fallen dramatically in recent years, so that Spain celebrates the tax freedom day in April along with other countries such as Bulgaria, Latvia, Romania, Slovakia, Ireland, Poland or Greece.

In fact, Spain is, after Ireland, the second country in the euro zone where tax collection fell the most in the last three years (14.5 percent), thus becoming also the state where the tax freedom day has improved the most. The surprising fact is that countries such as Italy, Portugal, Finland and even Greece, with GDP growth rates as low as those of Spain in the last four years, have managed to control the falls in tax collection below 2 percent, at the same time that Spain supports a drop of more than 14 percent.

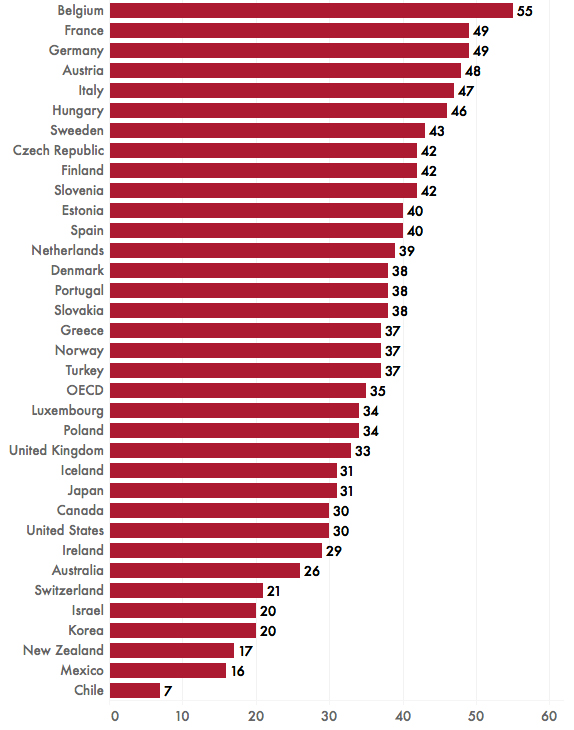

Graph 5. Tax burden on income

On the other hand, countries such as Ireland or Latvia, which register significant falls (above 20 percent), do so at the cost of declines in GDP from 14 percent to 19 percent. Therefore, it can be said that the Spanish case is exceptional, since no European country with positive growth rates —over the last four years— has suffered such a drastic contraction in tax collection.

The case of Spain

Spain is an exception in the European landscape, due to its high levels of shadow economy and the rigidities of its labor market. The property-based housing policy has limited interregional mobility, while collective agreements designed for the manufacturing economy during the 1950s restrict labor mobility. All this, together with a tax system with very high tax rates for the level of income in Spain, helps the shadow economy increase, while maintaining high unemployment rates and keeping tax collection low.

We must not forget that tax pressure is closely related to the collection capacity of the tax authority. Spain is the best example of how rising tax rates drops collection. Nor should we forget that the tax pressure of an economy is measured in relation to its GDP, which encompasses much more than the sum of wages and salaries.

Whereas in recent years tax pressure Spain has been decreasing, the tax burden on labor income —i.e. tax effort— continues to increase. Proof of this is the latest report of the Organization for Economic Cooperation and Development (OECD), Taxing wages, which has just confirmed that the tax effort in Spain is high. Spain was, after Iceland, the second OECD country that increased the most the tax burden on labor last year, reaching 39.6 percent of income. The OECD taxes into account, in addition to personal income tax, tax deductions and Social Security contributions by the company and the worker. Last year, the increase in tax pressure has been 1.36 percent, so that the tax pressure on work is still much higher than the OECD average (34.9 percent) and the differential continues to increase year after year.

The only chance Spain has today is probably to improve tax collection and reactivate the economy through lower taxes. This would lower labor costs, making hiring and job creation more attractive. All this would result in an increase in the number of taxpayers and, therefore, in an increase in revenue.

Methodology

The Tax Freedom Day is an indicator that translates tax effort into the number of work days that citizens and businesses need throughout the year to pay taxes. It is calculated by comparing tax revenues with GDP. Tax revenues considered include direct and indirect taxes collected by the Central, Autonomous and Local administrations and Social Security contributions.

The data required to calculate the tax effort is based on the income liquidations of each of the public administrations, but for the most recent data, estimates and/or forecasts of liquidations have been used and, in some cases, income forecasts of the budgets of CCAA and municipalities. For the geographical distribution of the execution of the social security revenue budget for 2009 and 2010, the methodology takes into account the number of Social Security affiliates in each Autonomous Community and a regional constant. In the case of GDP, data consists of forecasts, advances or estimates. Therefore, from one year to the next there may be changes in the date pointed out as Tax Freedom Day.

Civismo has used the same methodology and a single source for the calculation of Tax Freedom Day for all EU member states, thus obtaining comparable international data although these do not always coincide with the Tax Freedom Day published by local organisations.

References

Taxing Wages 2009-2010, OCDE 2011

Tax Foundation http://www.taxfoundation.org/

Adam Smith Institute http://www.adamsmith.org/tax-freedomday/

Institute for Market Economics

Liberální Institut