This study addresses the economic impact that will result from the tax scenario that is being outlined in the Draft Law on the Tax on Certain Digital Services (IDSD in Spanish), if it obtains the support of Congress within the framework of the General State Budget Project for 2019. This project is born from the initiative of the Spanish Government —led by the Socialist Party— to establish a new taxation structure, which fully affects the digital economy. With it, it advances and transcends the debates that are being held in this regard within the OECD and the European Commission.

The creation of this tax is an extraordinary challenge for the digitalisation of the economy of our country. It is necessary to start from the fact that it is a booming market, with annual growth rates that do not fall below double digits, and whose thrust will inevitably be slowed down if obstacles are put into its breeding ground: a flexible and dynamic environment that allows developing economies of scale, that is, the touchstone on which any expansion process rests.

Spain justifies the implementation of these measures on the grounds that digital taxation constitutes an objective of the European Commission, as evidenced in the explanatory statement of the aforementioned draft of the law. There, there is reference to the proposal for a EU Directive presented on March 21, 2018, at the request of the Council, related to a common tax system that seriously damages the income from the provision of certain digital services.

The main purpose of this tax proposal is to “correct the inappropriate allocation of tax rights that occurs as a result of the lack of recognition by the current international tax regulations of the contribution of users to the creation of value for companies in the countries where they carry out their activity».

However, this being said, the Bill itself recognises that, with the IDSD Spain anticipates the conclusion of the discussions about it that will take place within the European Union, and thus adopting «a unilateral solution» that allows it to «immediately exercise taxation rights that legitimately correspond to it». This legislative initiative has not being agreed with other member states and it is also being undertaken without a clear plan on the consequences that it may entail.

Therefore, the taxation of multinationals and, especially, of the digital sector, is the protagonist in the public debate. Indeed, the European Commission proposed to tax digital services through the income generated, given that, in its view, companies operating in this sector would be paying less taxes than they should and, therefore, the new assessment would help to create a “fair tax” on these activities [1].

Although there has been a consensus in the EU institutions regarding its implementation and design date —it would be postponed until 2020—, Spain, together with Italy and the United Kingdom, has demarcated itself from the European line, and intends to establish this digital tax already in 2019. To achieve this, the Spanish Government has put in place the legislative machinery, in order to approve it even if the same did not happen with the General State Budgets for 2019. Through this route, it would have an additional source of income , which would allow it to balance the accounts according to the deficit targets agreed with the European Commission.

Given this new scenario, full of uncertainties for long-term economic progress, it is necessary, on the one hand, to analyse the consequences that the new digital tax will have on the sector and, therefore, on the Spanish economy. And, on the other, it must be quantified its economic impact on a series of variables, focusing on the value chain of the digital sector:

(i) We estimate a cost on the margins of the digital services industry in Spain of 178.14 million euros per year. The most affected segments, by degree of importance, are digital advertising and intermediary lines of products and services.

(ii) The digital tax will annually subtract 2.01 percent of profitability on sales on average, although with an asymmetric behaviour according to the business segment —depending on the rotation of services.

(iii) The final consumer will assume a third of the final tax payment, while the remaining two thirds fall on intermediaries against margins, investments and employment. The most affected companies would be the SMEs, since they are the intermediaries in the retail segment, where the ability to pass the tax on to the consumer is lower.

(iv) The investment capacity of the sector will be reduced by 0.5 percent, in terms of a lower net result of these companies.

(v) The damage to the consumer (individuals + freelancers + SMEs) amounts to 0.474 euros per capita on average for each digital product taxed —with special emphasis on online transactions and data sharing.

Introduction. Digital services market in Spain

Analysing the so-called digital economy is a complex issue. It is not trivial to determine what is meant by the digital services market, especially when separating what activities can be considered as such. Therefore, in order to establish a clear and objective delimitation, before proceeding to quantify the economic impact that will result from the creation and entry into force of the IDSD, it is worth studying the digital market in which it will operate. This will help to better understand in which environment you will interact and the possible repercussions. An x-ray that can be done from two perspectives:

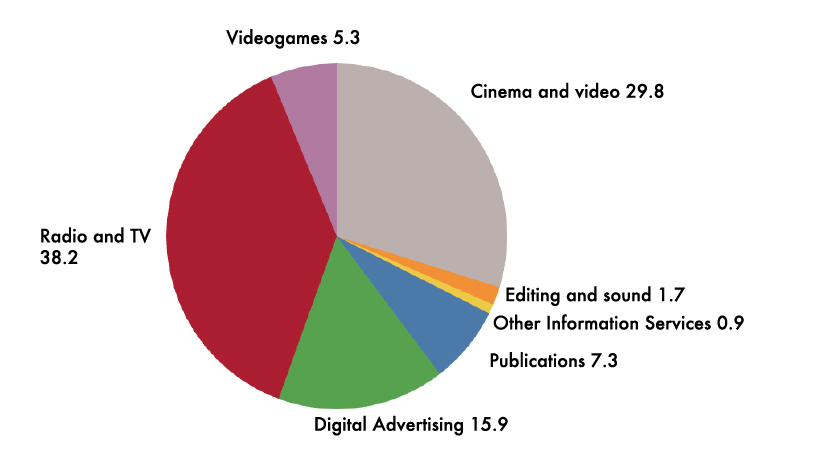

On the one hand, there is the perspective of the various activity branches. According to 2017 data from the National Observatory of Telecommunications and the Information Society (ONTSI in Spanish), the agents that conform this market are, mainly, the radio and television companies whose turnover represents 38.2 percent of the total; those of cinema and video, with 29.8 percent; and those of digital advertising, with 15.9 percent. Publications, videogames, editing and sound, and the other information services follow the abovementioned ones.

Graph 1. Distribution of the turnover by branches of activity (2017)

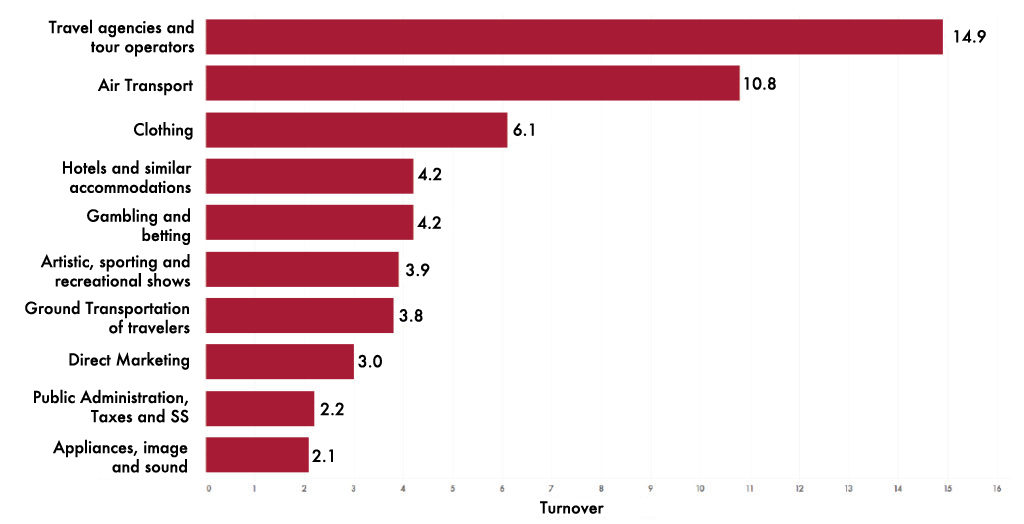

The other perspective from which to address this issue is that of the nature of electronic commerce transactions. From this second approach, the activities with more weight in the total turnover are, according to 2018 data from the National Commission of Markets and Competition (CNMC in Spanish), those from travel agencies and tour operators (14.9 percent), and those of air transportation (10.8 percent), followed by others that do not reach double digits, such as garments, gambling and betting, hotels and similar accommodation, art shows, sports and recreation, passenger land transport, direct marketing, public administration, taxes and social Security, or appliances, image and sound. Within this list, the sectors that would be most affected by the IDSD are, logically, the ones that grow the most in cumulative average variation rates. Namely, activities related to transportation and hotels.

Graph 2. Distribution of the turnover by the nature of electronic commerce transactions (2018)

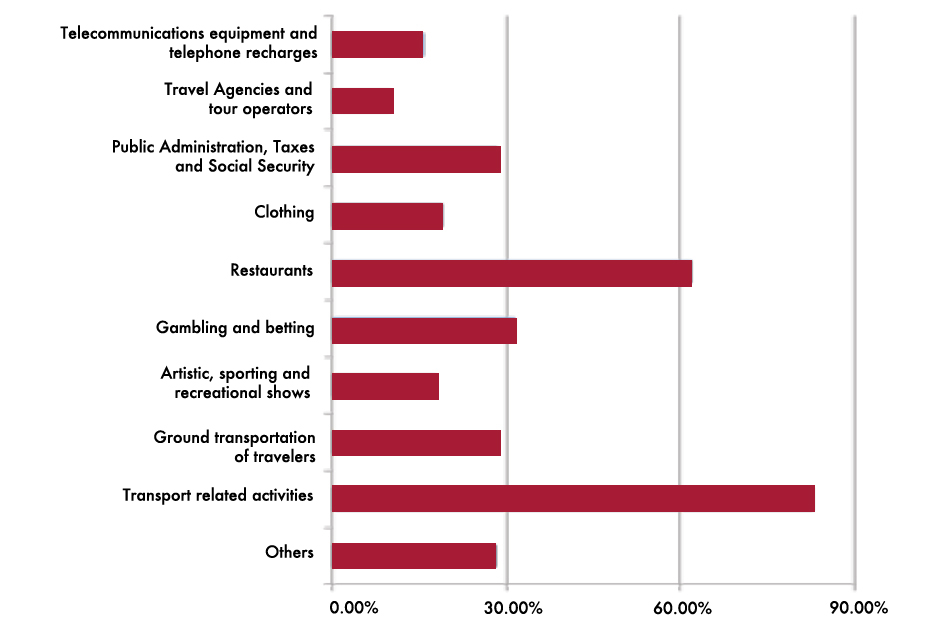

These have grown in the last four years at cumulative average rates of 82.96 percent and 61.97 percent, respectively, according to data published by the CNMC.

Graph 3. Cumulative annual growth rates of the turnover by the nature of electronic commerce transactions (2014-2018)

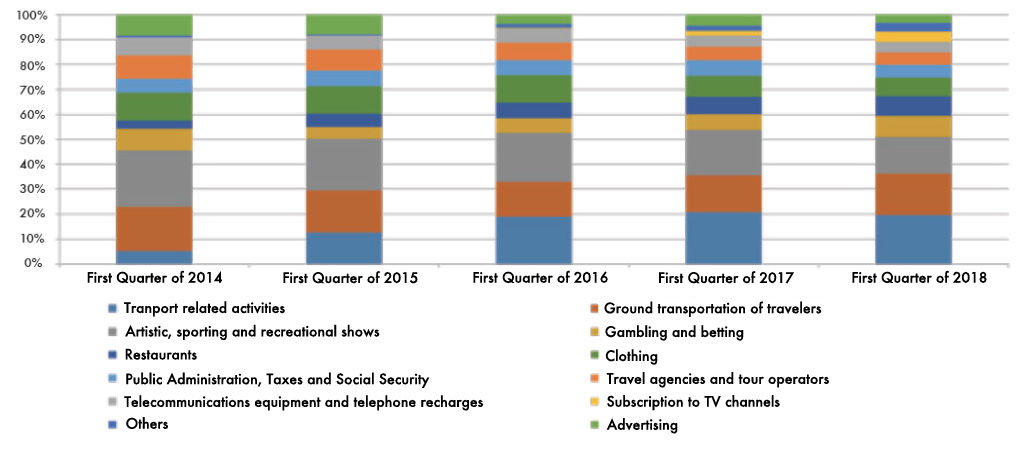

Graph 4. Distribution of the turnover by the nature of electronic commerce transactions (2014-2018)

Finally, to complete the photograph of the digital services market in Spain, the main figures that create the sector, provided in 2017 by ONTSI and IDATI, must be taken into account, based on data from the end of 2016. Thus, the turnover amounts to 9,834 million euros, which implies an annual growth of 4.8 percent and the increase in the turnover of digital advertising services was 21.5 percent. Moreover, the number of companies that compose it is 9,749; generates 39,491 direct jobs, that is, 38 percent of the entire content industry; and the investment in digital content amounts to 605 million euros.

What is the new digital taxation?

What is the digital taxation proposed by the Government?

Once the robot portrait of the digital market has been made, it is appropriate to dissect in what terms the new tax has been designed, in order to assess its suitability and to what extent it may be harmful within its scope.

As can be seen from the Bill, the IDSD taxes the online advertising services, the online intermediation services and the sale of data collected from the information provided by the user. The taxpayers are companies whose net turnover amount exceeded 750 million euros last year, and those whose income from services subject to the tax in Spain are above the three million euros last year. This tax will be required at the rate of 3 percent, and the settlement period will coincide with the calendar quarter.

This way, the IDSD resembles the one proposed by the European Commission in the draft Directive of March 2018 described above, although it diverges in some points and presents certain aspects that can be controversial and problematic. First, despite being conceived as an indirect tax, it introduces elements of direct taxation, such as the fact that it is intended to identify the companies that bear it. Secondly, it will be implemented without having reached a consensus among the member countries, which would avoid loss of competitiveness.

Finally, the tax takes for granted the existence of a series of technical means, necessary to exercise adequate tax control and ensure proper implementation, which, today, are difficult to articulate, even in countries more advanced than Spain in terms of prevention and tax supervision.

The taxes paid by a digital company

The debate is based on an assumption: the low level of taxation that digital companies bear today. However, empirical evidence shows that digital companies pay effective rates of the main taxes similar to those of traditional companies. In addition, costs associated with double taxation fall on them, in businesses where it is difficult to determine the flows of financing, investment and the creation of added value.

The challenge of “data” taxation

The debate on data taxation is extraordinarily relevant, given that, in a scenario of technological revolution such as the current one, a parallel tax revolution would be necessary to modernise tax techniques, to define taxable actions, and to implement a tax policy favourable to data development. Not surprisingly, it seems out of the question that this constitutes the fourth productive [2] factor, or even the fifth, if human capital is taken into account. Like the latter, these are the only ones capable of generating increasing returns to scale. With this foundation, the tax debate presents two points worthy of attention: on the one hand, where the taxable events take place and, on the other, where the taxes that are deducted from each of them must be collected. In this regard, there are two opposing positions. On the one hand, there is the perspective of those who think that taxes should be charged individually by country —at the risk of generating double taxation—, establishing inspection controls and tax obligations even though the digital service is provided from abroad —the most significant case is that of taxation according to where the servers, cloud service and data centers are located, as they are trying to implement in India [3]. On the other hand, there are those who believe that a taxation of a direct nature must be exchanged for an indirect one, borne by the final consumer. This would be partially the thesis of the European Commission reflected in the Fair Taxation on a Digital Economy package, as it also defends more control over corporate taxation.

Whether one opts for one way or the other, it is clear that the digitalisation of the economy will face tax pressure whose intensity will depend on how the conception of governments over it evolves. It is desirable, as we will show later, a supranational agreement at the OECD level, so as not to create unnecessary distortions that can curb the digitalisation process and, above all, put the European digital industry in danger and in worse conditions to compete in the world.

Throughout the discussion there are certain aspects of geopolitical confrontation that cannot be forgotten. Thus, the European digital industry is strongly influenced by the great superpowers: United States and China. Therefore, one of the underlying debates is to use a tax like the one being discussed to reduce the foreign power over the digital development of the old continent. However, it does not take into account a fundamental issue today: the existence of value chains that go beyond the borders of a State or a union of countries.

Economic impact of the new digital taxation

Impact of digital taxation: evaluation and results

Given the real tax situation of the digital company in Spain, the deficiencies and design failures of the IDSD under the current draft law entail a series of important consequences in the medium and long term, although, in this study, its measurement is carried out in the short term:

(i) Economic cost along the value chain, focusing attention on prices and margins

(ii) Impact on the demand for digital services (especially in its elasticity)

(iii) Overall impact and on the collection of the tax

Economic cost along the value chain: costs on trade in digital services

From the most up-to-date data from sources such as the CNMC, ONTSI, INE, Eurostat, the Bank of Spain, etc., it can be seen how the IDSD would have a negative impact on digital commerce within Spain and on purchases of nationals from abroad —that is the part of the genuinely indirect tax—, since the one made with a non-resident counterpart in our territory is not taxed. Therefore, discrimination is being exercised between the domestic market, which accounts for 36.5 percent of all digital transactions, and the foreign market. In practice, this is equivalent to the imposition of a tariff [4].

Graph 5. Proportion of the turnover of the digital industry according to the origin and destination in the Spanish market (2018)

(i) Economic cost along the value chain: impact on the margins of digital companiesRegarding the impact on the margins of the sector, understood as those of companies located in the third quartile by size (those subject to the tax), along the entire value chain, the application of a 3 percent IDSD tax would imply, ceteris paribus, a reduction of the gross margin on the net amount of the turnover of up to 2 percent (from the current 66.8 percent to 64.8 percent), according to data from the Central de Balances of the Bank of Spain [5].

Taking into account the total turnover (8,855 million euros), the decrease in margins amounts to a total of 178.14 million euros per year. Although there is the possibility of neutralising this effect via price, it will always depend on the type of customer, both intermediate and final. In addition, the model predicts that two thirds of the tax cannot be passed through this channel, so companies will have to assume it. In terms of gross economic profitability, assuming that the sales [6]figure is not modified, this translates into a symmetric decrease of 2.01 percent.

(ii) Economic cost along the value chain: impact on the behaviour of the demand for digital services

The calculation of the impact of the IDSD can also be approached based on the characterisation of the consumer, considering for this purpose individuals, SMEs and freelancers who are at the end of the value chain, as well as the estimation of their average expenditure in each product or service demanded, and of the behaviour of the demand based on the prices and the quantities offered.

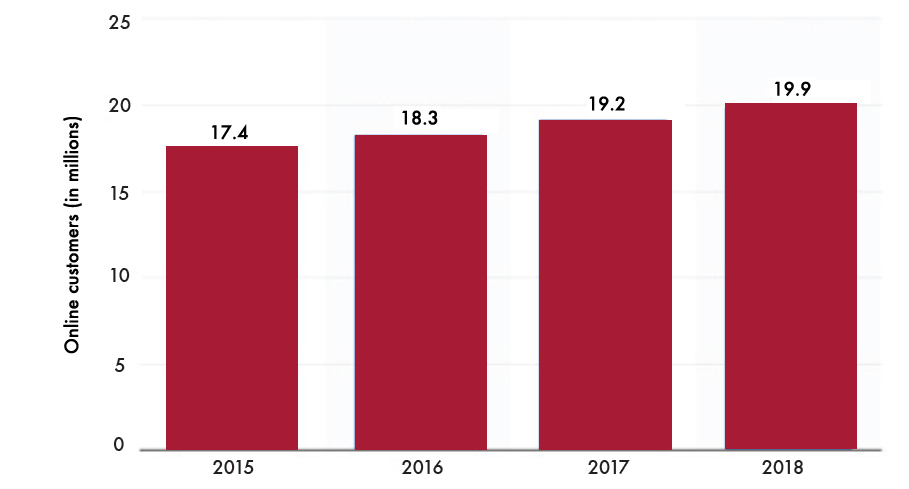

According to Statista data, the target audience to which the finalist digital services are directed in Spain amounts to about twenty million people, due to annual growth of around 900,000 customers. All of them perform several online purchase actions, in which an average price of 37.30 euros per acquisition is estimated.

Applying the 3 percent rate at which the tax is to be set, the final consumer would suffer an extra cost of 0.47 euros per purchase, which raises the average amount to 37.77 euros. It entails, therefore, an inflationary effect on goods that, although still of minor importance in the shopping cart, are increasing their weight, as shown by the INE Family Budget Survey.

Graph 6. Number of online consumers in Spain

However, the impact on the demand for digital services can be attenuated, thanks to the elastic nature of the demand curve due to the high number of substitute goods and services in each segment; especially in advertising and intermediation, both online and offline.

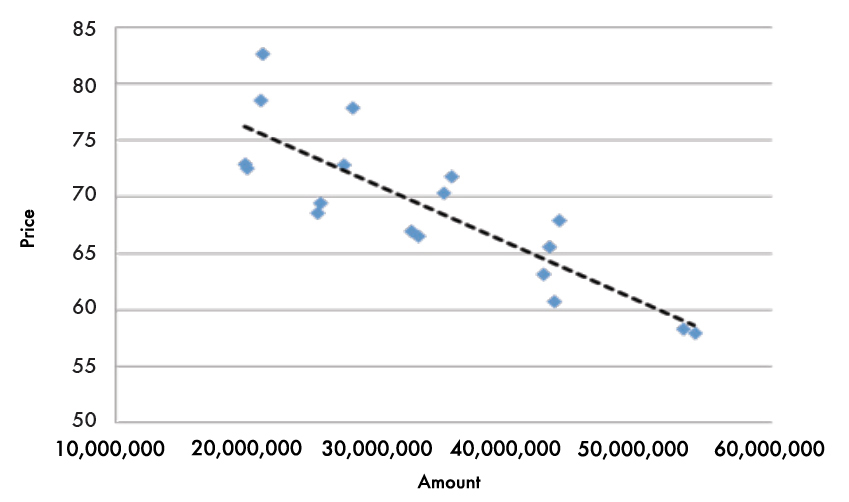

Graph 7. Estimation of the demand curve for digital services in Spain

Once the demand curve is estimated, the overall impact on the value chain is calculated based on the costs previously quantified in terms of trade, margins and demand. Taking into account all the variables, the total costs of the tax are computed using the deadweight loss method, determining three basic areas:

(i) Loss of well-being in the final consumer (individuals + self-employed + SMEs)

(ii) Loss of efficiency in producers, intermediaries and distributors of digital services (calculated as an impact on the margins of the industry)

(iii) Changes in investment and employment decisions, especially multinationals

Graph 8. Estimation of total costs along the value chain

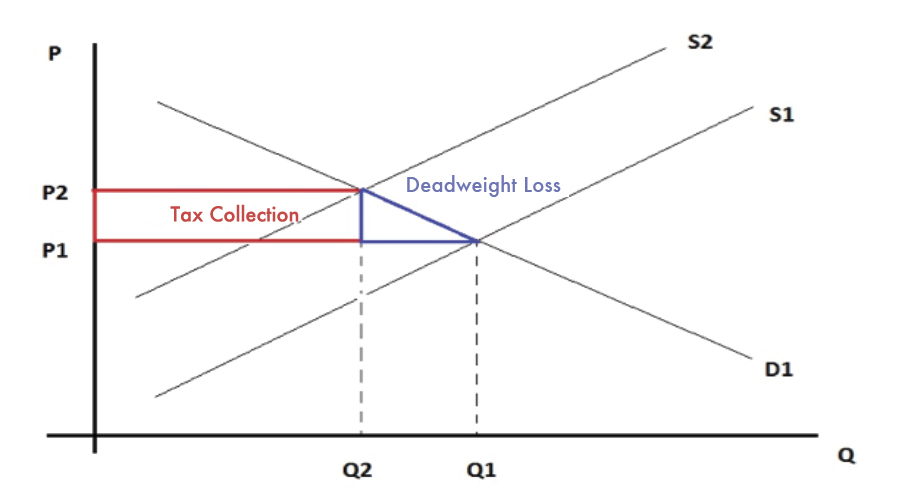

The area that comprises the difference between the variation of the consumer’s surplus and that of the producer is the “deadweight loss” that implies a competitive market equilibrium in which the quantity produced is lower and the price is greater. Thus, taking into account the variation in production and price (3 percent higher due to the effect of the ad-valorem tax), the deadweight loss would rise to 302.6 million euros in the first year of application.

At the same time, there is another area that determines the estimation of tax collection, which, applying the calculation of the area of a rectangle, is 929.12 million euros: substantially less than estimated in the Bill, and around the consensus figures that the market is currently handling.

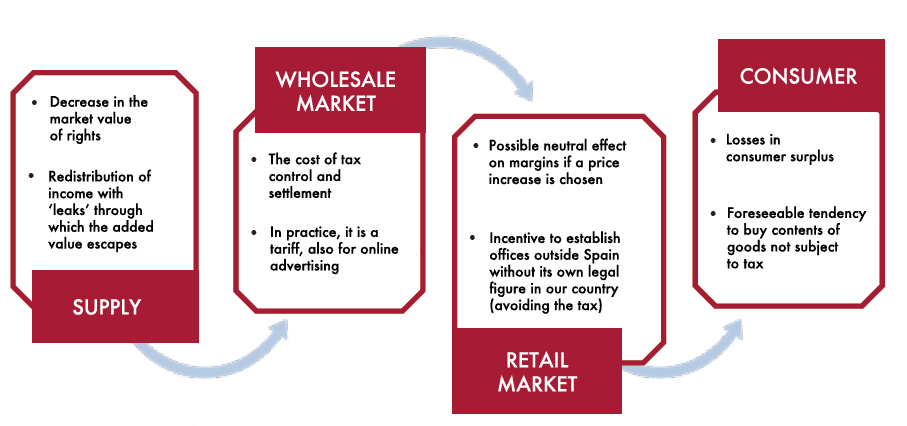

At this point, it is necessary to refer to the importance that tax collection and tax control costs will have for the Spanish Treasury, especially when the Ecofin is contemplating the limitations that the member states would have to avoid possible cases of fraud and tax avoidance. Even taking into account the change incorporated in the Bill that contemplates the deduction of the IDSD in the Corporate Tax, the technical and human resources of the Tax Authority would be insufficient to control the operations of large companies that have operating subsidiaries in Spain but whose services are provided from abroad. In sum, total losses would be distributed along the value chain, adopting various manifestations depending on the actors affected. Thus, on the supply side, the value of rights would decrease, and income would be redistributed, and part of the added value would escape through “waterways”. For the wholesale market, costs would be incurred for control and settlement of the tax, and, in practice, a tariff would be created, also for online advertising. In the case of the retail market, despite the fact that the effect on the margins could be neutralised by raising prices, companies would be encouraged to establish offices outside of Spain in order to avoid taxation. As for the consumer, it will, foreseeably, tend to acquire contents of those goods not subject to the tax.

Graph 9. Total costs along the value chain

Conclusions

From this analysis it is possible to affirm that clear negative effects derive from the application of the IDSD, which could be summarised as:

(i) Permanent losses in the value chain

(ii) Incentives for lower investment and relocation of innovation

(iii) Economic damages on demand

(iv) A substitution effect of the contents taxed by those which are not

As a reaction to the legislative proposal, and in order to mitigate or avoid its harmful consequences for the digital services sector, this study proposes a strategy based on the following props:

(i) Coordination at the European level to achieve a common tax framework

(ii) Data contribution and added value by the sector during the parliamentary deliberation period

(iii) Disclosure among the public opinion of the damage caused by the tax

References

Central de Balances del Banco de España. Datos de cierre de 2016.

“Informe anual del sector de los contenidos digitales en España”. ONTSI, 2017.

Comercio Electrónico. CNMC, datos de la última actualización (1T 2018).

«Uso y actitudes de consumo de servicios digitales». ONTSI, 2017.

“The Proposed EU Digital Services Tax”. Copenhaguen Economics.

“Estudio de la economía digital: los contenidos y los servicios digitales”. Ametic, PwC & U-tad.

Hufbauer, G. C., and Lu, L. (2018): “The European Union’s Proposed Digital Services Tax: A De Facto Tariff”, 18-15 PIIE Policy Brief, Peterson Institute for International Economics, June 2018.

“India finds a new way to tax Google, Facebook”; Economic Times of India, 17t December 2018.

Jones, S. (2012). “Why ‘Big Data’ is the fourth factor of production” Financial Times, 27t December 2012.

“¿Qué impuestos pagan las empresas? La OCDE constata una caída de Sociedades en todo el mundo”, El Boletín, 17/01/2019.

Santacruz Cano, J. (2017): “La factura fiscal de las empresas en España. La fiscalidad real de las empresas en el final de la campaña del Impuesto de Sociedades”, Civismo.

European Commission (2018). “Proposal for a Council Directive on the common system of a digital services tax on revenues resulting from the provision of certain digital services”.

[1] European Commission (2018), “Proposal for a Council Directive on the common system of a digital services tax on revenues resulting from the provision of certain digital services”. https://ec.europa.eu/taxation_customs/sites/taxation/files/proposal_common_system_digital_services_tax_21032018_en.pdf. Also, see OECD (2015), ‘Addressing the Tax Challenges of the Digital Economy: Action 1 – 2015 Final Report‘, OECD Publishing, Paris; and OECD (2018), ‘Tax Challenges Arising from Digitalisation – Interim Report 2018: Inclusive Framework on BEPS’, OECD Publishing, Paris.

[2] Jones, S. (2012). “Why ‘Big Data’ is the fourth factor of production” Financial Times, 27th December 2012. https://www.ft.com/content/5086d700-504a-11e2-9b66-00144feab49a

[3] “India finds a new way to tax Google, Facebook”; Economic Times of India, 17th December 2018: https://economictimes.indiatimes.com/news/economy/policy/localisation-heat-data-bank-here-may-help-government-debit-taxes/articleshow/67120911.cms

[4] Hufbauer, G. C., and Lu, L. (2018): “The European Union’s Proposed Digital Services Tax: A De Facto Tariff”, 18-15 PIIE Policy Brief, Peterson Institute for International Economics, June 2018. https://piie.com/system/files/documents/pb18-15.pdf

[5] Considerando el margen bruto que la Central de Balances calcula para las empresas que se sitúan en el tercer cuartil de la distribución con datos de 2016 (publicados en 2017). Ver referencias estadísticas.

[6] A partir de la expresión de la rentabilidad económica se considera invariante la cifra de ventas a corto plazo (limitada capacidad de reacción de empresas y consumidores ante cambios de corto plazo).