Introduction

The situation on the Spanish labor market is being debated by specialists and policy makers with respect to two central questions: on the one hand, the type of employment that is being generated following the crisis and, on the other hand, the medium-to-long term sustainability of this job creation. In terms of the jobs created, the principle characteristics of the current labor market identified by many analysts are the prevalence of temporary employment, poor productivity, and low salaries. However, there is evidence that calls into question this description of the labor market and encourages deeper study. The present paradigm does not generally qualify as ’precarious’ since there are different underlying realities that indicate that added value is being generated in the most dynamic areas of the economy. The contribution of the tourism industry (alongside large corporations) as a motor for Spanish economic growth is crucial in the evolution of the factor of work and in the progressive reduction of unemployment.

This working paper intends to shed light on the evolution of the Spanish labor market, its fundamental determinants, and the effects of productivity for the tourism sector, highlighting models in regions where this sector experiences strong growth. In the first chapter, we analyze what types of contracts were agreed in the first quarter of 2017 in our country, including what the working hours were, categorizing according to sector. In the second chapter, we emphasize the tourism sector. In the third chapter, we introduce the hotel industry within the tourism sector for our economy. In the fourth chapter, we analyze labor productivity in the regions of the Balearic Islands and Aragon before concluding in chapter five.

Characteristics of the Spanish labor market: contracts and working hours

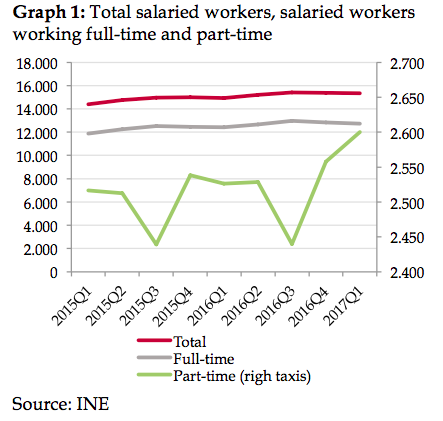

The most recent Economically Active Population Survey (Spanish acronym: EPA), published by the National Statistics Institute (Spanish acronym: INE), shows that 18,438,300 people had a job in Spain during the first quarter of 2017. Salaried workers (those who receive a salary in exchange for labor that they do regularly) represent 83 percent of these people. Graph 1 visualizes how approximately 90 percent of salaried workers in Spain work full-time and the rest, about 10 percent, work part-time. A priori, these statistics may seem favorable, but in terms of job creation it is more complicated.

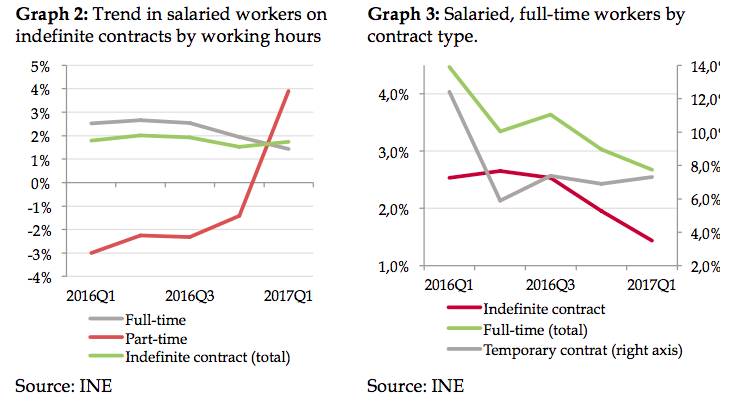

The first quarter of 2017 saw 408,700 new jobs compared to the same period the year before. As shown by Graph 2, the growth in salaried workers who work part-time has risen to surpass that of indefinite contract workers. Meanwhile, full-time workers keep increasing in numbers, but at a slower pace. Out of the total of new indefinitely contracted workers in the first quarter of 2017, a mere 1.4 percent were on full-time contracts, while the part-time equivalent has risen to 4 percent. In other words, in the three first months of the year, only 1.4 percent of the total increase in full-time employment consisted of indefinite contracts, as opposed to 7.3 percent of fixed term contracts (see Graph 3).

The European Commission’s council recommendation on the Spanish 2017 National Reform Program, which includes its opinion on the 2017 Program for Stability, has already warned us. It identifies temporary employment as a primary problem in the Spanish labor market. The Commission acknowledges that job creation has been strong in recent years and that unemployment has fallen rapidly, even though it remains high, particularly among the young and the low-skilled. It also recognizes that labor market reform and wage moderation have been important drivers of this recovery and of the gains in competitiveness made in recent years, despite the employment rate being one of lowest in the EU.

It warns that “Spain has one of the highest shares of temporary employment in the EU, and many temporary contracts are of very short duration. Transition rates from temporary to permanent contracts are very low in comparison to the EU average. The widespread use of temporary contracts is associated with lower productivity growth (including through lower on-the-job training opportunities), poorer working conditions and higher poverty risks. The recent labour market reforms seem to have had a mildly positive effect in reducing segmentation between permanent and temporary contracts, and the ongoing reinforcement of labour inspections is showing positive results in addressing the abuse of temporary contracts. However, some features of the Spanish labour market may still discourage hiring on permanent contracts, including uncertainty in case of legal dispute following a dismissal, along with comparatively high severance payments for workers on permanent contracts. Moreover, the system of hiring incentives remains scattered and not effectively targeted at the promotion of open-ended employment. Although it has recently established a working group on the quality of employment, Spain has not yet developed a comprehensive plan for fighting labour market segmentation, following the 2014 agreement between the government and social partners.”

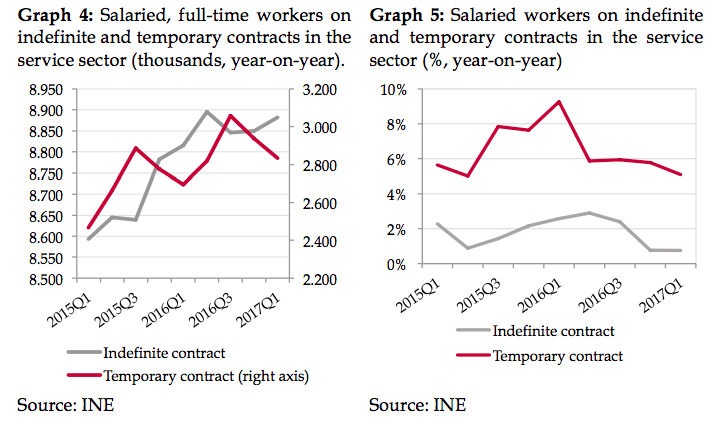

Added to this examination are problems in education, such as early school drop-outs, the high rate of course retakes among students, and elevated teaching costs, which adversely affect the potential for productivity growth in the long term. The employability of the university-educated remains relatively low: “The reduced mobility of students and academic staff, limited traineeships’ opportunities, lack of incentives and the rigidity of university governance remain obstacles to cooperation with business on education or research. Analyzing by economic sector, the service sector made up 76 percent of total employment in Spain in the first quarter of the past three years. In terms of contract type, this sector held 73 percent of total full-time job positions, whereas the figure for part-time contracts reaches up to 90 percent. In the service sector, the number of salaried workers on indefinite contracts is greater than the number on temporary contracts: some nine million people compared to three million, respectively (Graph 4). With regards to growth rates, seen in Graph 5, the rate for workers on temporary contracts reaches 9 percent, compared to a maximum of 3 percent for those on indefinite contracts.

The role of tourism in the Spanish labor model

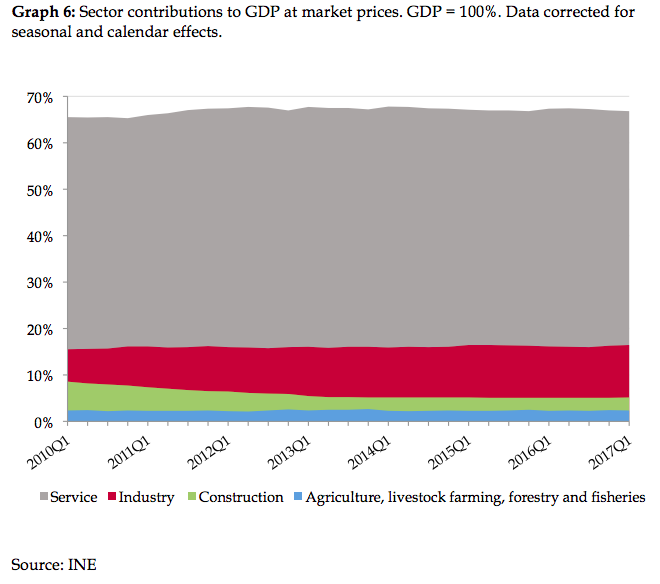

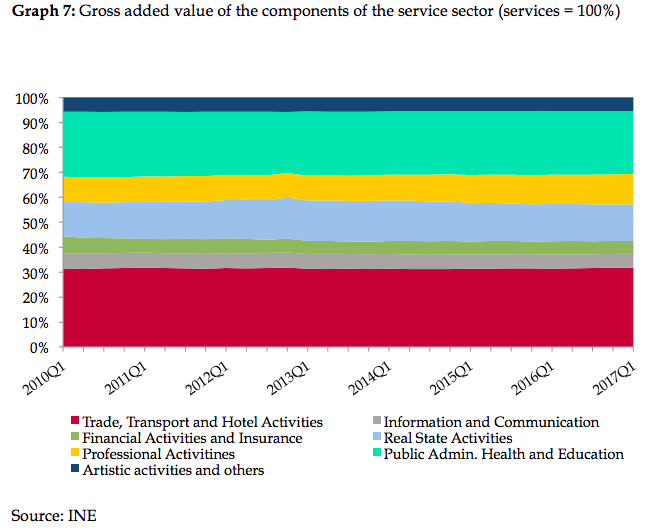

Within the service sector, tourism plays a critical role in our country. It represents a significant portion of GDP (Graphs 6 and 7) and contributes to a large extent to the development of our economy. It is therefore not surprising that the largest group of people who are active in the service sector work in tourism. It is because of this great dependency that the Spanish labor market features such a large number of temporary contracts in the service sector. Focusing on the breakdown of the service sector (Graph 7), we see that the “Commerce, Transport, and Hotel Industry” category makes up 35 percent of the sector and contributes the most to sector growth, followed by “Public administration, Public health and Education.”

When the World Economic Forum named Spain the most competitive country in the world in matters of tourism, it also highlighted its weaknesses. Out of the 14 areas ranked, Spain stands out in a negative manner for its business climate, which includes conditions for entrepreneurship, investment and recruitment (labor market), and in its international openness (measured mainly through prices, in which developing countries will win).

The recommendations and warnings by the European Commission and the World Economic Forum share a theme: our deficient labor system, both for employers (because of scant ways of hiring) and for employees (because of temporariness and the short duration of contracts).

The hotel sector

The factors of determination of competitiveness in the tourism sector can be comparative as well as competitive. The prior can be related to the resources at the tourist destination, including climate, landscape, cultural wealth and distance from visitors’ countries of origin. The competitive advantage, by contrast, encompasses factors ranging from price levels to sector structure, including how businesses are managed and characteristics of the business environment, according to the Bank of Spain. In this case, the analysis will target the competitive advantage of the hotel sector: their management, their price levels, and their characteristics in the Balearic Islands and Aragon. These areas are of particular interest since they are the autonomous communities that have the highest and lowest labor productivity in the tourism sector, respectively, according to our calculations based on data from INE’s Hotel Occupancy Survey. It considers the rate of occupancy, the price index, and indicators of profitability.

The improvement in economic growth in Europe allows the markets in Germany, France, and elsewhere to keep adding to the expansion of tourism in the Balearic Islands. However, the effects of Brexit could threaten the current favorable conditions.

Fewer British tourists as an eventual result of a weaker pound compared to the euro is not the only risk. There could be a change in the trend that led tourists to prefer Spain to other destinations because of geopolitical tension. This means that although business owners in the tourism sector can stay calm, they should not under any circumstances limit themselves to offering just sunshine and beaches. Instead, they would have to improve their productivity in order to offer a higher-quality service to the tourists and, in so doing, increase their competitive advantage.

Productivity in the tourism sector: the case of the Balearic Islands

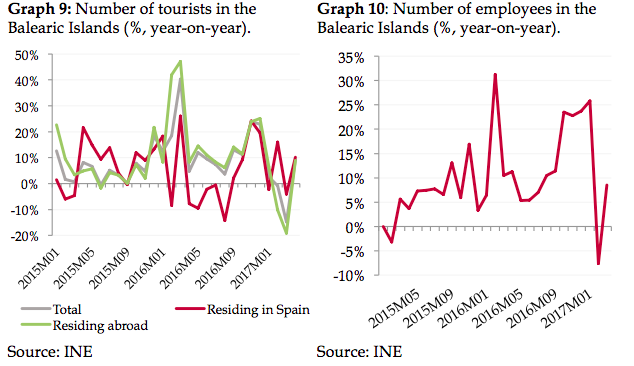

In 2016 and early 2017, the flow of tourists to the Balearic Islands returned to developing favorably as people were attracted by natural resources, convenient infrastructure, and security. As seen in Graph 7, year-on-year growth was exceptional last year, especially in March, which saw 40 percent more tourists, mainly from abroad. The inflow of this type of travellers to the archipelago is unstoppable. In 2015, the total number of foreign tourists grew by 10 percent; in 2016, by 11.6 percent.

Turning to tourists’ spending, the Balearic Islands experienced a 10.5 percent increase in direct spending thanks to visitors from abroad. However, the first months of 2017 do not follow this trend: growth rates for February and March are lower, or even negative, due to fewer foreign tourists. In April, the rising trend returned and it was expected to improve during the summer holiday season.

As the number of visitors has increased, so has the economic activity of the hotel sector. The number of employees has grown rapidly to meet the arrivals of tourists in search of an enjoyable vacation. The seasonal nature of the sector is reflected in the temporariness of employment contracts. The number of employees rose notably in 2016, overtaking the peak number from the previous year in March. In the same month this year, owing to fewer visitors in total, the sector does not employ as many people as it did in 2016.

Having established the correlation between job creation in temporary positions and the number of tourists going on vacation in the Isles, it is fitting to ask: are employers combining the factors of production in a way that maximizes performance?

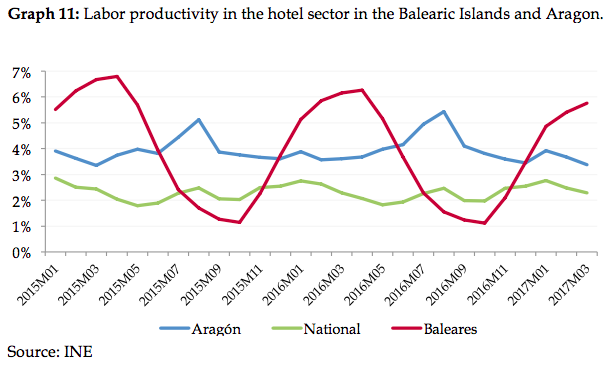

Making calculations using data from INE’s Hotel Occupancy Survey, it is possible to measure the productivity of the tourism sector. To analyze partial productivity (labor productivity), we multiply the average daily room charge by the average duration of stay and by the number of travellers before dividing it by the number of employees in the sector. We see as a result that productivity in hotels in the Balearic Islands is highly seasonal. During spring and summer, it is very low: about 1.0 percent. In the cold season, it rises to between 4.0 and 6.0 percent as these months see many international tourists leaving. It is suitable to add that the growth rate in the number of tourists, during high and low season alike, has continued rising at a positive rate compared to previous years, probably because of lower prices during the low season and higher temperatures than in foreign visitors’ native countries.

By contrast, in Aragon, productivity is more stable. It is greater during the summer months, unlike in the Balearic Islands. This is due to tourism in Aragon taking place to a larger extent during the winter months, driven by ski resorts. It should be emphasized that the hotel productivity of this region exceeds the national average, signaling better utilization of employed staff in its hotels.

In Spain, hotel productivity fluctuates between 2 and 2.5 percent over the course of a year. This national average remains stable due to the coexistence of various types of tourism in our country, meaning that the number of tourists roughly balances: it benefits from snow sports in winter and the promise of sun and beaches in summer. In spite of this, the service sector in our country does not boast great productivity, seen mainly in the tourism sector that is characterized by seasonal climate conditions.

Conclusion

Out of the employment generated in Spain in the first quarter this year, salaried, full-time workers make up a mere 1.4 percent whereas the corresponding number of part-time workers is 4 percent. Additionally, out of the total increase in full-time workers, just 1.4 percent secured indefinite contracts as opposed to 7.3 percent for fixed term contracts. These differences between growth rates in full-time and part-time employment and between fixed and indefinite contracts are even more pronounced in the service sector.

Since the tourism sector, marked by its seasonal characteristics, is a motor for the Spanish economy, it is no coincidence that more temporary contracts are signed than indefinite ones in terms of job creation. Analyzing the cases of labor productivity through our measure of partial productivity, we find that Aragon benefits from labor productivity that is higher than the Spanish average, while the Balearic Islands experience very low levels during the tourist high season of spring and summer and elevated levels during the winter months. In order for productivity in the Balearic Islands to be less cyclical, employers should prepare better ahead of mass tourist arrivals. Also, using new organizational methods and acquiring new technologies, they can become less labor-intensive.

References

BBVA Research. Situación Baleares: 2017. March 2017.

Caixabank Research. La economía de Illes Balears: diagnóstico estratégico. 2008.

European Commission. Recommendation for a Council Recommendation on the 2017 National Reform Programme of Spain and delivering a Council opinion on the 2017 Stability Programme of Spain

Exceltur. Perspectivas Turísticas. Valoración empresarial del primer trimestre y expectativas para la Semana Santa y el segundo trimestre de 2017. April 2017. Nº60.

Instituto Nacional de Estadística. Coyuntura Turística Hotelera (EOH/IPH/IRSH). May 2017